You're usually not asking about contractor insurance requirements in a calm moment. You're staring at a contract, a bid package, or a certificate request that suddenly feels more legal than operational. You want a simple answer, but there usually isn't one.

That's the first thing to understand. Contractor insurance requirements aren't one fixed checklist. They change based on state rules, the client you're working for, and the kind of job you're doing. If you can read those three signals correctly, you can usually tell what's required, what's negotiable, and what will get you blocked before work even starts.

Table of Contents

- The Core Four Insurance Policies Every Contractor Needs

- Why Insurance Requirements Vary By State and Project

- Decoding Coverage Limits and Umbrella Policies

- How to Read and Verify a Certificate of Insurance COI

- Beyond the Basics Important Endorsements to Look For

- Actionable Steps for Coverage and Verification

The Core Four Insurance Policies Every Contractor Needs

Most confusion disappears once you separate the major policies by the problem each one is built to handle. Think in terms of who got hurt, what got damaged, and how the loss happened.

What each policy actually does

General liability is the policy people usually mean when they ask, “Are you insured?” It covers third-party bodily injury and property damage. If your crew damages a client's property or someone gets hurt because of your operations, this is the policy that usually responds.

Workers' compensation covers job-related injuries to your employees. It protects the worker, and it protects the business from taking that loss straight onto its own balance sheet. In the United States, workers' compensation is required by law in nearly all states, and commercial auto insurance is mandatory in nearly every state, according to construction insurance guidance for contractors.

Commercial auto handles vehicles used in the business. If a truck, van, or other work vehicle is involved in an accident during business operations, this policy is the one that matters. A personal auto policy often isn't built for that exposure.

Professional liability, often called E&O, is different from general liability. It addresses financial loss tied to professional services, design decisions, plans, advice, or errors in technical judgment. It matters more in design-build, consulting-heavy, and specification-driven work than in straightforward labor-only jobs.

Why these four drive most compliance requests

General liability and workers' compensation sit at the center of most contractor insurance requirements because they're tied to access. Licensing boards, public entities, universities, and larger private owners often won't let you onto the job without them.

That's why the request often starts with policy names and limits, not with a discussion of your actual risk philosophy.

Practical rule: If a policy affects your license, your ability to bid, or your ability to get on site, treat it as operational infrastructure, not optional protection.

One useful way to remember the split:

- General Liability: Damage or injury to other people and their property

- Workers' Compensation: Injuries to your employees

- Commercial Auto: Accidents involving business vehicles

- Professional Liability: Loss tied to advice, design, or technical errors

A lot of newer businesses make one of two mistakes. They either buy only the minimum they can find, or they buy a package without checking whether it fits their trade. Neither works well. A roofer, HVAC company, restoration firm, and design-build contractor can all look “insured” while carrying very different gaps.

If you're hiring a trade for a major exterior project, this is one reason screening matters early. A guide on how to find a good roofer is useful because the quality question and the insurance question usually show up together.

Why Insurance Requirements Vary By State and Project

There's no single national template for contractor insurance requirements. The rules are layered, and each layer can change what counts as acceptable coverage.

State law sets the floor

The legal baseline usually starts with the state. Licensing rules, workers' compensation requirements, vehicle laws, and trade-specific registration standards all sit there first. That's the floor, not the ceiling.

Commercial general liability minimums can be surprisingly low in some places. A state-by-state overview of general liability requirements notes that state minimums can fall between $50,000 and $300,000, while residential service work often lands around $500,000 to $1,000,000, and commercial or public-project work frequently requires $1,000,000 per occurrence and $2,000,000 aggregate. If your limit doesn't match the requirement, you can lose the license, permit, or award even if your policy is technically active.

That's why “I have insurance” often means very little by itself.

The client and the job raise the bar

Once the state baseline is met, the client's contract usually determines the actual requirement. A homeowner replacing a furnace typically won't demand the same paperwork as a university, municipality, developer, or general contractor on a public job.

The work itself matters too. A painter working inside an occupied home usually presents a different risk profile than a roofing contractor, restoration company, or HVAC installer cutting into building systems. Jobs with delayed loss discovery, structural implications, public access, vehicles on site, or design responsibility tend to trigger tougher requirements.

Here's the practical decision framework:

| Driver | What it changes | What to watch |

|---|---|---|

| State law | Licensing and minimum legal compliance | Policy type, active status, minimum limits |

| Client type | Contractual limits and documentation | Higher limits, added endorsements, COI timing |

| Scope of work | Trade-specific exposure | Auto, completed operations, professional liability |

A residential service call and an institutional construction project can both require “general liability,” but they are not asking for the same thing in practice.

People hiring contractors run into a version of this too. Insurance expectations for a simple home repair aren't always the same as those tied to broader property exposure. That's one reason many people also look closely at homeowners insurance coverage before work starts, especially when the project could affect a roof, HVAC system, or major building component.

What works is reading the requirement in layers. Start with state law. Then read the contract. Then compare both to the actual risk of the job. What doesn't work is assuming the policy that got you through one project will satisfy the next one.

Decoding Coverage Limits and Umbrella Policies

The numbers on a policy aren't decoration. They tell you how much capacity is available when a loss hits, and whether the policy is even usable for the job you're trying to win.

What per occurrence and aggregate actually mean

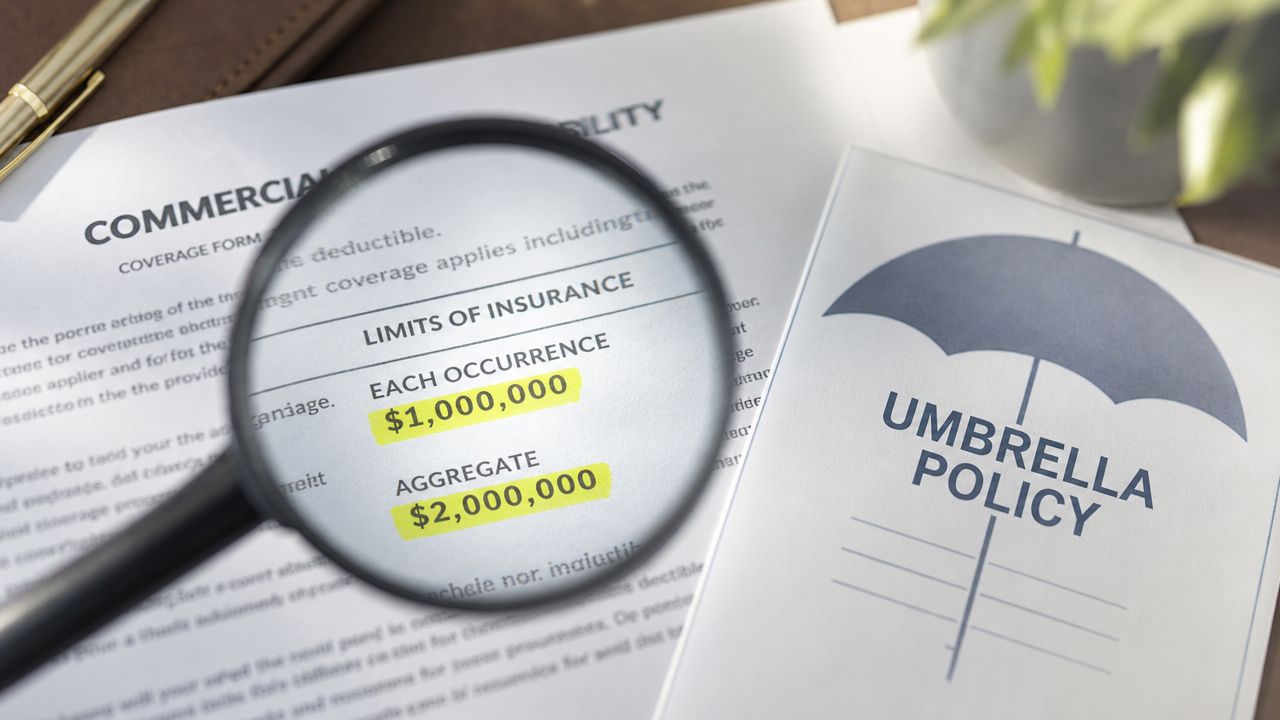

When you see $1,000,000 per occurrence / $2,000,000 aggregate, read it this way:

- Per occurrence is the maximum the policy can pay for one covered incident.

- Aggregate is the maximum the policy can pay across the policy term.

If a contract asks for $1,000,000 per occurrence and your policy tops out below that on a single claim, you don't meet the requirement. If the aggregate is too low, you may have enough protection for one claim but not enough for a year with multiple losses.

A certificate that looks close is still noncompliant if the contract language is exact.

When umbrella coverage becomes necessary

Many contractors first encounter umbrella coverage when they move into institutional or public work. They had enough insurance for smaller jobs, then a contract lands on the desk requiring limits that sit above the primary policy.

The scale of the market reflects how established this has become. IBISWorld estimates the Contractors' Insurance market at $13.7 billion in 2026, and notes that universities and public agencies often require umbrella coverage reaching $5,000,000 or more for major work in a layered compliance structure, according to IBISWorld's Contractors' Insurance industry overview.

A few real-world examples from institutional procurement make the pattern clear:

- Kansas State University: $1,000,000 each occurrence, $2,000,000 aggregate CGL, $1,000,000 auto liability, and $1,000,000 professional liability where design/build applies

- Tufts: $1,000,000 CGL, $1,000,000 auto liability, and in some cases $5,000,000 umbrella plus $2,000,000 cyber insurance

Don't treat umbrella coverage as a luxury line item. For some contracts, it's simply the only way to meet the limit structure without rebuilding the entire insurance tower.

What works is matching limits to the job before pricing or signing. What doesn't work is assuming your broker can “fix it later” after award. Sometimes they can. Sometimes the carrier, cost, or timing won't cooperate.

How to Read and Verify a Certificate of Insurance COI

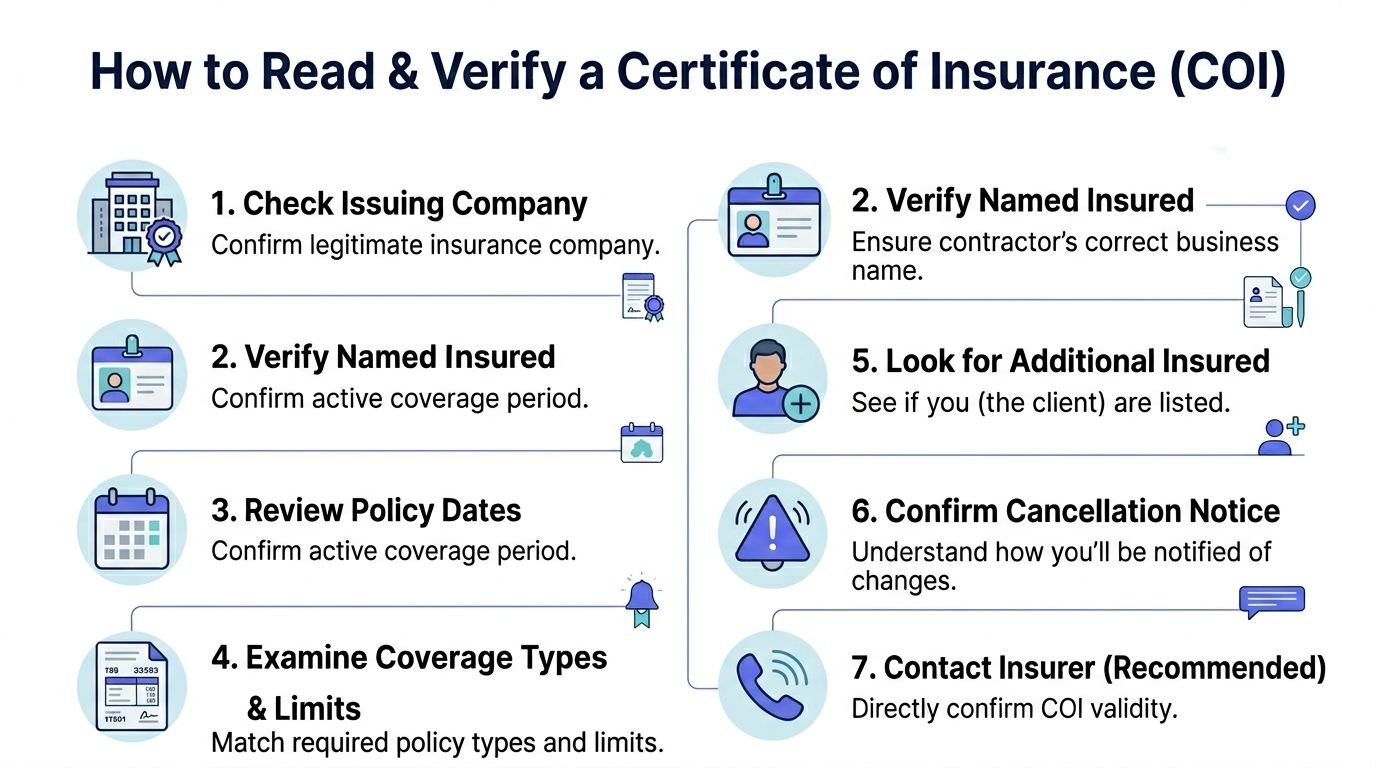

A certificate of insurance is a snapshot, not a guarantee. It tells you what policies are reported to be in place on the date issued. That makes it useful, but only if you know what to check.

What to check first

Start with the basics. If these are wrong, the rest of the document doesn't help much.

Named insured

The business name on the COI should match the legal entity signing the contract. Not a DBA that isn't on the agreement. Not the owner's personal name unless that's the insured business.Carrier information

Check that the issuing insurance company is listed clearly. If the COI feels improvised or incomplete, ask questions.Policy dates

Coverage needs to be active for the project period. A COI with limits that look perfect but expiration dates that lapse mid-project creates a real compliance problem.Policy types and limits

Match the COI to the contract line by line. General liability, workers' compensation, auto, umbrella, professional liability. Compare the exact limits requested.

What separates proof of insurance from real protection

Many owners and many contractors get burned. A COI can show active insurance and still fail the contract.

A key detail in public and municipal contracting is that project owners often must be named as additional insureds. Some requirements also call for separate proof for all subcontractors. The Federal Acquisition Regulation guidance on insurance requirements reflects that asking whether a contractor is insured is insufficient. The status of the owner and the proof for subs can determine whether a claim is covered cleanly or turns into a dispute.

Use this verification checklist:

- Certificate holder is correct: Your company or ownership entity should be listed accurately.

- Additional insured status is addressed: Don't assume the COI alone proves it. Ask for the endorsement when the contract requires it.

- Subcontractor proof exists: If subs are on the job, confirm whether they're covered under the prime's policy or need separate certificates.

- Cancellation language is understood: Know how notice works, and don't rely on assumptions.

- Limits match the contract exactly: Close isn't enough.

If the contract requires additional insured status and the endorsement isn't there, the contractor may be compliant only on paper.

One more practical point. Timing matters. Some jobs require proof before work begins. Others require it before contract award, and that can decide whether a bid stays alive at all. Waiting until mobilization to sort out documentation is a common and expensive mistake.

Beyond the Basics Important Endorsements to Look For

The policy limit gets the attention. The endorsement often decides whether the policy fits the job.

Completed operations is where many policies fail the real test

A contractor can carry a standard-looking general liability policy and still leave the client exposed after the job is done. That's why products/completed operations matters so much.

Institutional insurance requirements often call for CGL that includes products/completed operations and contractual liability, because post-completion losses are a serious source of construction claims. Indiana University's published insurance requirements note common structures such as $1,000,000 per occurrence and $2,000,000 aggregate for CGL, with statutory workers' compensation and employers' liability around $500,000, while some public contracts go higher. Their requirements also highlight why completed-operations coverage matters for delayed-loss trades such as roofing, HVAC, and restoration in these institutional insurance standards.

If a roof leaks months later, if HVAC work contributes to a later building issue, or if restoration work fails in a way that only shows up after closeout, this is the part of the policy everyone suddenly cares about.

The loss that matters most may not show up during the job. It may show up after handover, when everyone assumed the paperwork was already settled.

Other contract endorsements that matter

A few endorsements show up again and again in stronger contracts:

- Additional insured endorsement: This extends certain liability protection to the owner, general contractor, or other required party. Asking for the COI alone isn't enough when the contract specifically requires the endorsement.

- Waiver of subrogation: This limits the insurer's ability to pursue recovery from a party the contractor agreed to protect under contract.

- Per project aggregate: This helps keep one project from competing with unrelated claims under the same policy aggregate.

- Primary and noncontributory wording: This can matter when multiple policies could respond and the contract allocates how coverage should apply.

What works is reviewing endorsements before signing, not after the first certificate request gets rejected. What doesn't work is assuming every CGL form contains the same post-completion and contractual features. It doesn't.

For owners, the key question isn't just “Do they have insurance?” It's “Does their policy include the endorsements this contract expects?” That's a much better filter.

Actionable Steps for Coverage and Verification

If you want a simple operating rule, use this one. Read the contract before you buy or approve the insurance. Most problems start when people reverse that order.

If you're the contractor

- Map your work first: Separate residential service, light commercial, public work, and design-build exposure. Different work streams often trigger different insurance requirements.

- Send contracts to your broker early: Don't summarize the requirements from memory. Forward the actual document and ask whether your current program meets it.

- Check endorsements, not just limits: A policy can show the right numbers and still miss completed operations, additional insured language, or other required terms.

- Track renewals and certificates actively: Expired proof can stop payment, delay site access, or kill a renewal application.

- Vet your subs like an owner would: Collect current certificates and confirm their coverage aligns with your subcontract.

If you're hiring the contractor

- Ask for a COI made out to your entity: That forces a more project-specific review than a recycled generic certificate.

- Compare the COI to the contract: Match named insured, policy dates, coverage lines, and limits.

- Request endorsements where required: Especially additional insured status and any project-specific wording.

- Don't ignore subcontractors: If subs are involved, ask how their insurance is being handled and documented.

- Screen the business itself: Insurance matters, but so do licensing, background checks, and reputation. A useful starting point is this guide to a contractor background check.

The businesses that handle this well treat insurance as part of job setup, not last-minute admin. The owners who handle it well don't stop at “yes, we're insured.”

If you want a simpler way to find a qualified pro without sorting through a crowded lead marketplace, Hand Vetted Co. matches you with one licensed, background-checked, highly rated professional at a time. You can also review How It Works, Our Standards, and the FAQ to see how the verification process works before you move forward.