You're probably at the same point many homeowners hit. The design looks good, the scope feels real, then the estimate lands and suddenly the project stops being about tile, shingles, or cabinets. It becomes about cash flow.

That's where renovation plans usually go sideways. Not because the project is bad, but because the financing choice is. Pick the wrong tool and you either overpay, move too slowly, or put your house at risk for a project that didn't require that level of risk in the first place.

The good news is that home improvement financing options are pretty straightforward once you sort them by project size, how fast you need the money, and what your finances look like today.

Table of Contents

- Your Project Is Planned How Do You Pay for It

- Cash vs Credit A Breakdown of Your Options

- Personal Loans and Credit Cards When to Use Them

- Home Equity Loans HELOCs and Refinancing

- Financing Options for Tougher Scenarios

- A Decision Framework for Choosing Your Financing

- Your Next Steps From Budgeting to Hiring

Your Project Is Planned How Do You Pay for It

A kitchen remodel feels exciting right up until you realize the cabinets, labor, permits, and surprises behind the walls all need to be paid for on a real timeline. Same with a roof. Same with HVAC. Same with a bathroom that started as “just a refresh” and turned into plumbing work.

This isn't a new problem. The U.S. has relied on renovation financing for a long time. HUD reports that more than 31 million loans have been insured under the FHA Title I program since 1934, and HUD also notes that home improvement expenditures “have doubled since 1970” in its historical review of the market, which tells you financing has been tied to home upgrades for decades, not just during high-rate or high-cost periods (HUD historical financing overview).

The first mistake is treating every project the same

A leaking roof and a dream kitchen shouldn't be financed the same way.

If your project is urgent, speed matters more than squeezing out the absolute lowest rate. If your project is large and planned well in advance, cheaper long-term borrowing usually matters more. And if your finances are tight, the best theoretical loan option might not be the one you can get approved for.

Practical rule: Match the financing to the job. Don't force the job into the financing you already had in mind.

The three questions that matter most

Before you compare lenders, answer these:

- How big is the project: Small repairs, mid-sized upgrades, and major renovations don't belong in the same financing bucket.

- How fast do you need the money: Emergency replacement jobs reward speed. Planned remodels reward patience.

- How much risk are you willing to take: Borrowing against your home can lower cost, but the tradeoff is obvious and serious.

That framework will narrow your options fast and keep you from wasting time on products that don't fit.

Cash vs Credit A Breakdown of Your Options

The cleanest way to think about home improvement financing options is this. You can pay with money you already have, borrow without using your house as collateral, or borrow against the value built up in your home. That's it.

Start with the least risky money

Cash is the cheapest option in the narrowest sense because you're not paying interest. But that doesn't automatically make it the smartest choice. Draining savings for a renovation and then getting hit with an insurance deductible, job interruption, or another repair is a bad move.

Borrowing can make sense if it protects your emergency cushion and keeps the project on schedule. Harvard's Joint Center for Housing Studies found that home improvement projects financed through home-secured credit averaged $10,622, and the same study reported that more than 20% of respondents used direct credit, including 19.1% using a regular credit card and 2.0% using a non-secured loan (Harvard JCHS financing study).

That tells you two things. First, people use a mix of tools. Second, bigger projects often push people toward equity-based borrowing.

A quick comparison table

| Option | Best For | Typical APR Range | Typical Loan Amount | Key Pro / Con |

|---|---|---|---|---|

| Cash or savings | Smaller planned projects, or people with strong reserves | N/A | Limited to what you have | Pro: no interest. Con: can wipe out liquidity fast |

| Personal loan | Small to mid-sized projects when speed and fixed payments matter | Varies by lender | Often used for smaller to mid-sized borrowing | Pro: fast and simple. Con: usually pricier than equity-based borrowing |

| Credit card | Very small purchases or short payoff windows | Varies widely | Revolving, depends on card limit | Pro: convenient. Con: expensive if the balance lingers |

| Home equity loan | Bigger one-time projects with a defined budget | Typically lower than unsecured credit | Often used for larger projects | Pro: fixed lump sum. Con: your home secures the debt |

| HELOC | Projects with phases or uncertain costs | Typically lower than unsecured credit, often variable | Flexible draw-based access | Pro: borrow as needed. Con: payment risk can change |

| Cash-out refinance | Major renovations when replacing the mortgage also makes sense | Depends on mortgage pricing | Larger borrowing tied to mortgage refinance | Pro: one consolidated loan. Con: resets your mortgage |

Recent lender data compiled by NerdWallet shows home improvement loan APRs ranging from about 7% to 36%, with average APRs over the last 30 days of 14.09% for excellent credit, 20.07% for good credit, 23.92% for fair credit, and 28.50% for bad credit. The same verified market snapshot notes loan sizes can range from $1,000 to $100,000, though many lenders cap borrowing at $30,000 to $50,000. Those figures are summarized in the verified data above.

Cheap money matters. But fit matters more. A slightly higher-rate loan you can fund quickly and manage comfortably can be a better decision than a lower-rate loan that delays the project or creates collateral risk you didn't need.

Personal Loans and Credit Cards When to Use Them

If your project is relatively contained and you need money soon, unsecured borrowing is usually the most practical path. No appraisal. No lien process. No waiting around while someone evaluates your home.

When a personal loan makes sense

Personal loans are best when you want fixed monthly payments and a fast close. That combination is hard to beat for roof repairs, HVAC replacement, appliance packages, flooring, smaller remodel phases, or any project where the contractor is ready and you don't want financing to be the bottleneck.

Wells Fargo markets fixed-rate home improvement loans with APRs from 6.74% to 25.99% and says funding can happen in days or even hours, which is exactly why unsecured loans are often the right answer when speed matters most (Wells Fargo home improvement loans).

Use a personal loan when these are true:

- You need speed: The project is urgent or the contractor is ready now.

- You want payment certainty: Fixed payments make budgeting much easier.

- You don't want to pledge your house: That matters more than chasing the lowest possible rate.

Where credit cards fit and where they go wrong

Credit cards are fine for materials, deposits, or smaller pieces of a project you can pay off quickly. They are not a smart way to carry a long renovation balance unless you have a very clear payoff plan.

The trap is convenience. Swiping for fixtures, finishes, and overages feels easy, right up until those charges hang around longer than planned. Then the flexibility that looked helpful turns into expensive revolving debt.

If you can't pay the card balance down on a defined schedule, don't use a credit card as your renovation loan.

My blunt take. Personal loans beat credit cards for most small to mid-sized projects because they force discipline. You get the money, you set the payment, and you stop pretending you'll “pay it off soon” while the balance keeps following you.

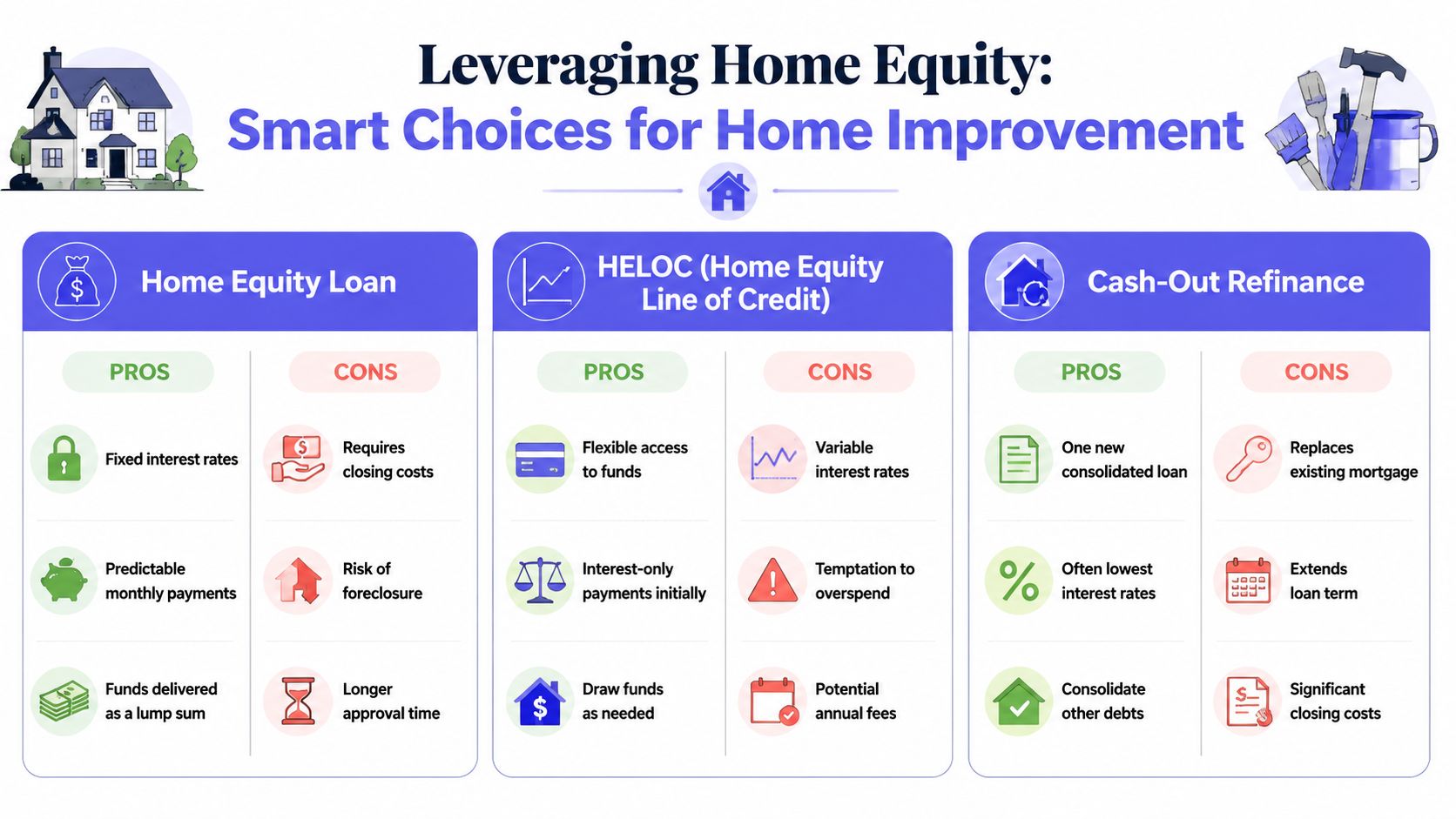

Home Equity Loans HELOCs and Refinancing

Once the project gets big, unsecured borrowing starts to lose its appeal. In this context, equity-based financing usually wins on cost.

Because the debt is secured by your home, lenders typically offer lower interest rates and longer repayment terms than unsecured credit, according to PNC's explanation of home improvement borrowing. PNC also makes the key downside clear. If you fail to repay, the home is exposed to foreclosure risk (PNC guide to home improvement loans).

The three equity options and who they suit

Home equity loan

This is the cleanest option for a project with a firm budget. You borrow a lump sum, usually repay it at a fixed rate, and know what the monthly payment is from the start. If your contractor quote is solid and the scope is unlikely to drift, this is often the easiest equity product to live with.

HELOC

A HELOC works better when the project will happen in phases or the final cost is less certain. You draw what you need when you need it. That flexibility is useful for staged renovations, but it can also encourage sloppy budgeting if you treat the line like free money.

Cash-out refinance

This one is bigger than a project loan. You replace your existing mortgage with a larger new one and pull cash from the difference. It can be smart, but only if the full refinance makes sense, not just the renovation. If you want to explore that route, compare lenders and refinance paths carefully through a mortgage refinance match.

The real downside people gloss over

Equity borrowing is cheaper for a reason. The house backs the loan.

That doesn't mean you should avoid it. It means you should only use it for work that's worth financing over a longer period and only after you've pressure-tested the payment. A major remodel, structural repair, or big-system replacement can justify that move. Cosmetic upgrades usually don't.

Here's my opinionated rule set:

- Choose a home equity loan if your bid is stable and you want predictable payments.

- Choose a HELOC if the job has phases and you need flexibility.

- Consider cash-out refinancing only if it improves the broader mortgage picture too, not just the renovation budget.

Financing Options for Tougher Scenarios

A lot of financing advice implicitly assumes you have strong credit, healthy equity, and a home in solid condition. Plenty of people don't. That doesn't make the repair less urgent.

Why standard advice fails a lot of people

This is the part most guides dodge. The products described as “flexible” often aren't very reachable when your finances are stretched or the property needs serious work.

The Urban Institute notes that renovation loans face a 43% denial rate, compared with 10.6% for purchase loans, and says many options still require a loan-to-value ratio of 80% or less, which shuts out a lot of people with limited equity (Urban Institute on renovation loan barriers).

Getting denied doesn't always mean the project is unreasonable. Sometimes it just means the standard lending box is too tight for the situation you're in.

What to look at if equity or credit is tight

If you have little equity, weak credit, or a property that isn't fully buttoned up, you may need to look at specialized renovation loans rather than the usual HELOC or standard refinance path.

That includes products like:

- FHA 203(k): Often discussed for homes that need substantial work because financing can be based on the value after repairs.

- HomeStyle and CHOICERenovation: Similar idea in spirit, but the process can be heavier and lender appetite can vary.

- Contractor-arranged financing: Sometimes useful, but read every term carefully and compare it against a direct personal loan offer.

These options can work. They can also be slower, more document-heavy, and more frustrating than the marketing suggests. If you're also dealing with property condition issues, it's smart to understand how coverage and repair obligations intersect by reviewing homeowners insurance coverage questions.

My recommendation is simple. If standard lending is a stretch, don't waste weeks pretending it isn't. Ask lenders up front whether they can handle limited equity, lower credit strength, or properties needing major repair. That saves time and protects your momentum.

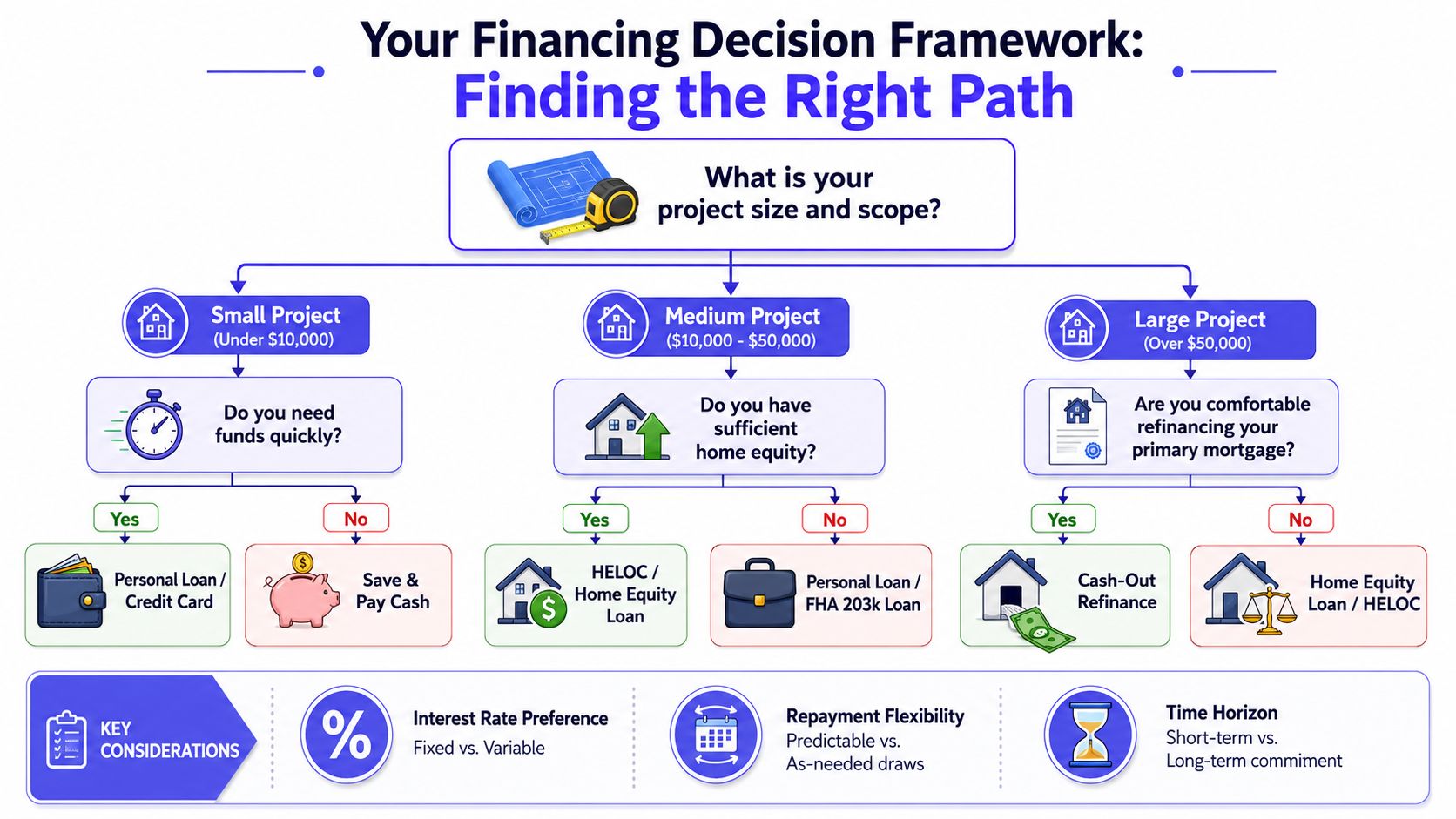

A Decision Framework for Choosing Your Financing

The best financing choice usually becomes obvious once you stop asking “What's the best loan?” and start asking “What fits this project and my finances right now?”

First decide based on project size and speed

Start with the job itself.

If it's a small project, paying cash is usually best if doing so won't drain your reserves. If cash would leave you exposed and the project can't wait, a personal loan is usually the cleaner move than trying to juggle balances across credit cards.

For a mid-sized project, ask whether you have enough equity and whether you want the house involved at all. If you do have equity and the project cost is meaningful, equity-based borrowing often deserves first look. If you don't, personal loans or renovation-specific products are usually more realistic.

For a large project, cost matters more because you'll feel the financing structure for a long time. That's where home equity loans, HELOCs, or possibly a cash-out refinance tend to make the most sense.

Then pressure test the choice against your finances

Run your shortlist through these four filters:

Can you handle the payment comfortably

If the payment only works in a perfect month, it doesn't work.

Do you need certainty or flexibility

Fixed payments are easier to budget. Flexible draw access is useful, but only if you stay disciplined.

Is the project urgent or planned

Fast funding matters more on emergency work than on a remodel scheduled months from now.

What are you putting at risk

Unsecured debt may cost more. Secured debt can cost you your home if things go badly.

Pick the loan that still looks smart after a delay, an overage, or a rough couple of months. Renovations rarely go exactly to plan.

If you want the short version, here it is:

- Urgent and smaller: personal loan

- Planned and larger with equity: home equity loan or HELOC

- Major project plus broader mortgage reset: cash-out refinance

- Low equity or tougher approval profile: renovation-specific programs first, standard products second

Your Next Steps From Budgeting to Hiring

You don't start with the loan. You start with the actual project number.

Do these in order

First, get a detailed written estimate. Not a vague verbal range. You need the scope, materials, labor, and likely allowances laid out clearly.

Second, decide whether the project is fixed-budget or likely to evolve. That alone will push you toward either lump-sum financing or something more flexible.

Third, compare financing based on total cost, payment comfort, and speed to funding. Don't get hypnotized by one number.

What to bring to a lender

Have this ready before you apply:

- A contractor estimate: Lenders want to know what the money is for.

- Your income and debt details: These details reveal approval reality.

- A clear scope: Roof replacement is different from an open-ended remodel.

- Your fallback plan: If the bid changes, know what you'll cut instead of blindly borrowing more.

And before you sign with any business, verify who you're hiring. A quick review of a contractor background check process can save you from financing a mess you'll have to pay to fix twice.

The smartest move is boring. Get the right estimate, choose the right financing structure, and hire the right pro. In that order.

If you want to shorten the messiest part of this process, start with Hand Vetted Co.. Handvetted matches you with one licensed, background-checked, highly rated professional for your project, not a pile of shared leads. It's a cleaner way to get a real estimate, compare your financing options with confidence, and move the job forward without the usual spam and guesswork.