You're about to open up walls, move plumbing, let strangers and subcontractors into your house, and spend real money improving the place. That's exactly when weak homeowners insurance coverage gets exposed.

Insurance is often treated like a box checked at closing. Then a renovation starts, a pipe bursts behind new cabinets, a worker gets hurt, or a contractor's mistake damages part of the house that wasn't even being touched. Suddenly the question isn't “Do I have insurance?” It's “Which policy pays, where are the gaps, and am I about to learn that the hard way?”

That matters more now because insurance is taking a bigger bite out of the household budget. The average U.S. household spent 2.09% of its income on homeowners insurance in 2022, nearly double the 1.19% share from 2001, according to the Insurance Information Institute's summary of Insurance Research Council data. If you're paying more, you should know exactly what protection you're buying before the first demo day starts.

Table of Contents

- Your Policy Is Your Project's First Line of Defense

- The Six Pillars of a Standard Homeowners Policy

- Decoding Your Policy's Value RCV vs ACV

- Plugging the Gaps Common Exclusions and Endorsements

- Insurance and Home Projects Protecting Yourself From Contractor Risk

- Navigating a Claim When Something Goes Wrong

- A Pre-Project Checklist to Manage Coverage and Costs

Your Policy Is Your Project's First Line of Defense

You sign the renovation contract. The start date is set. Materials are ordered. Then your insurer asks a question that homeowners should have considered first: has the risk at the property changed?

It has. A home project changes the insurance picture fast. Vacant rooms, exposed framing, temporary wiring, stored materials, new subcontractors, and interrupted utilities all create situations your old assumptions may not survive.

A standard policy can still be your first layer of protection, but only if you treat it like a living contract instead of a forgotten PDF. If your kitchen remodel turns into a whole-home gut job, your existing homeowners insurance coverage may no longer match the house's condition, value, or exposure.

Don't wait for a claim to learn that your policy was built for a finished, occupied home, not a property in the middle of construction.

Renovations also create confusion about responsibility. If a contractor damages your house, you might assume their insurance pays. Maybe. If your own property is damaged by a covered peril during the project, your carrier may still be involved. Sometimes both policies matter. Sometimes each insurer points at the other first.

That's why I tell people to stop thinking in terms of “Do I have coverage?” and start thinking in terms of “Which policy covers which risk, under what conditions, and with what limits?” That framing is a lot less comfortable, but it's the right one.

What changes during a renovation

A project can affect your insurance in a few ways:

- Your home may be worth more to rebuild: New finishes, added square footage, and upgraded systems can make your old dwelling limit outdated.

- Your risk profile shifts: Open walls, active trades, and material delivery create more chances for loss.

- Responsibility gets split: Your policy, the contractor's liability policy, and sometimes specialty construction coverage each handle different problems.

If you only remember one thing from this section, remember this: before work starts, call your insurer and describe the project in plain language. Don't sanitize it. “Minor update” is how people create ugly claim disputes later.

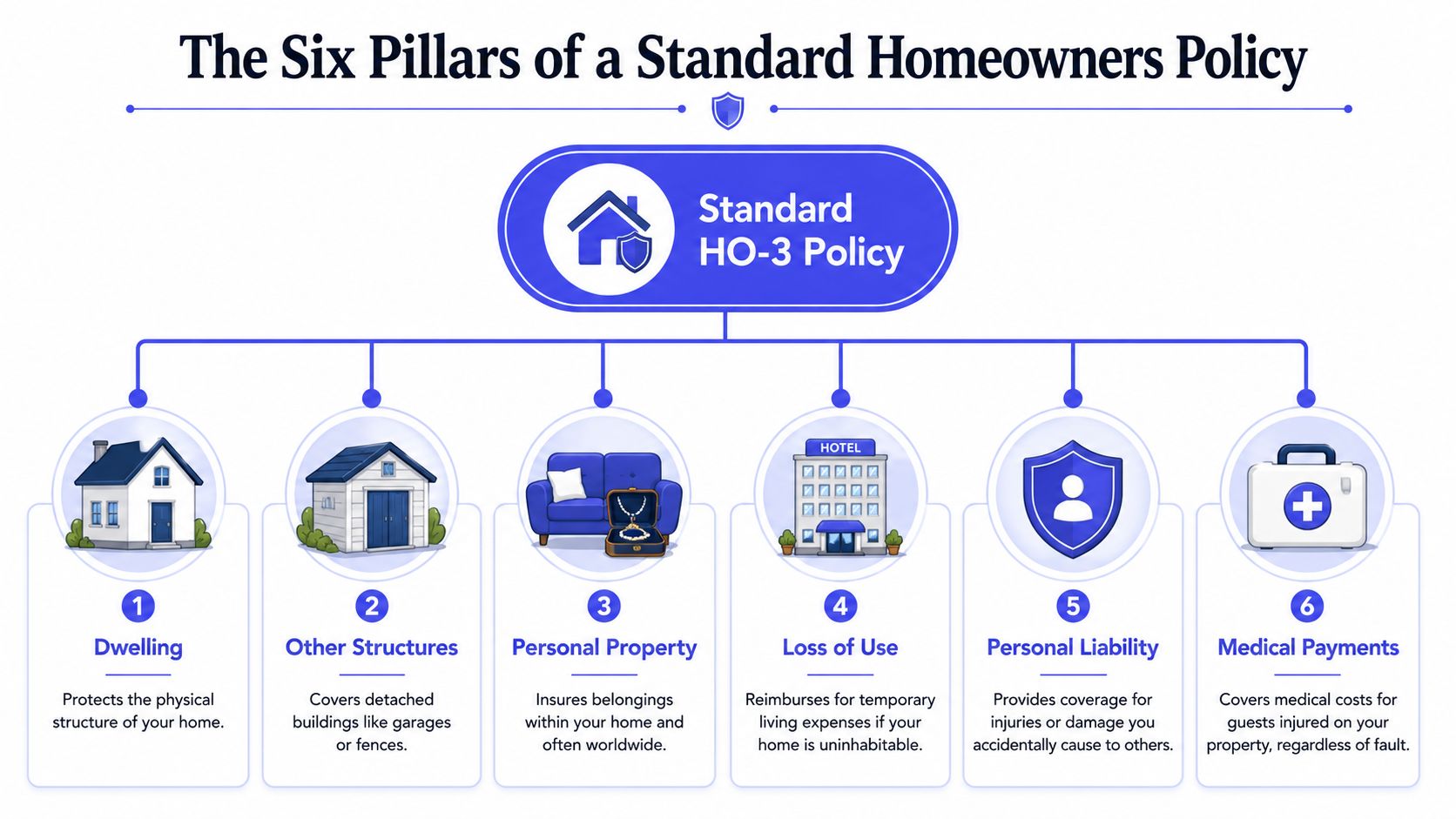

The Six Pillars of a Standard Homeowners Policy

Homeowners know they “have home insurance.” Fewer can tell you what's inside it. That's a problem, because renovations put pressure on every major part of the policy.

A standard homeowners policy is a package deal with core coverage for the home itself, personal belongings, liability protection, and additional living expenses if you're displaced, while still excluding major perils like flood and earthquake that usually require separate policies, according to the Insurance Information Institute's homeowners insurance basics guide. If you're shopping or reviewing options, a home insurance match through Handvetted can help you compare with an actual professional instead of guessing from ad copy.

What a package policy actually means

Think of the policy like a house with separate structural pieces. One section protects the building. Another protects what's inside. Another protects you if someone claims you caused harm. They work together, but they are not interchangeable.

That matters during a remodel because damage to cabinets, flooring, temporary housing costs, and an injury claim won't all pull from the same bucket. People lump it all together. Insurers don't.

The six parts that matter day to day

Here's the practical version of the six pillars.

| Pillar | What it usually does | Why it matters during a project |

|---|---|---|

| Dwelling | Covers the physical house | This is the section most likely affected by increased rebuild cost |

| Other Structures | Covers detached structures like fences or a detached garage | A project can damage areas outside the main house too |

| Personal Property | Covers belongings | Contents may be moved, stored, or exposed during work |

| Loss of Use | Helps with temporary living expenses if the home can't be lived in after a covered loss | Critical if a major incident interrupts the project and forces you out |

| Personal Liability | Helps if you're legally responsible for injury or damage to others | Claims can arise from project-related conditions on your property |

| Medical Payments | Covers smaller guest injury medical costs regardless of fault in many policies | Useful for minor incidents, but don't confuse it with full liability protection |

A few points people miss:

- Dwelling is not market value: It's about what it costs to repair or rebuild the structure.

- Personal property is not just “stuff inside the house”: It can matter even more during a renovation because items get shifted, stored, and sometimes damaged in transit or by dust and water.

- Loss of use is the quiet hero: If a covered loss makes the house unlivable, this part can matter more than people expect.

Practical rule: Read the declarations page first, then the exclusions. The declarations page tells you how much coverage you bought. The exclusions tell you where your assumptions can fail.

For renovation planning, I'd add a seventh mental category even though it isn't one of the standard pillars: what your policy does not cover. That's where expensive surprises usually live.

Decoding Your Policy's Value RCV vs ACV

People get distracted by premium and ignore the payout method. That's backwards. The premium matters, but the claim settlement method decides whether a loss feels manageable or financially brutal.

This is also where rising costs hit hard. Recent reporting says home insurance premiums were up 24% nationwide as coverage gaps widened, tying higher costs to affordability-driven underinsurance, where policy limits haven't kept pace with rebuilding costs, as noted in National Mortgage Professional's report on widening coverage gaps.

Limits, deductibles, and the number that hurts

Your coverage limit is the maximum the insurer will pay under that section of the policy. Your deductible is the amount you absorb before coverage kicks in.

During a renovation, both numbers matter more because repair costs can jump after upgrades, and small losses become common. If your dwelling limit was barely adequate before the project, it can become obviously inadequate after one.

The deductible deserves a blunt point. If you choose a deductible you can't comfortably pay from savings, you didn't really transfer the risk. You just bought a policy that starts helping after the moment you're already stressed and short on cash.

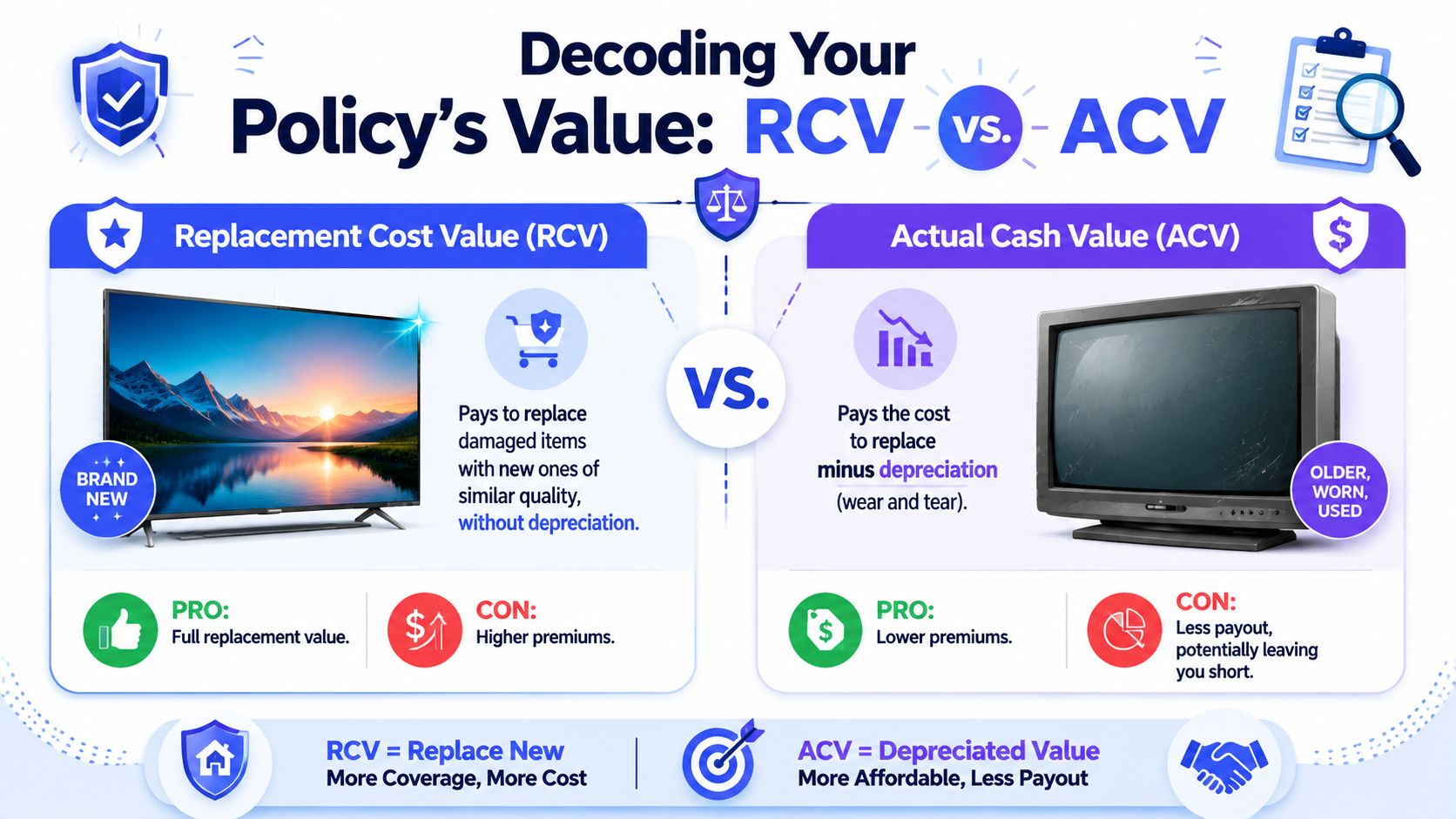

RCV and ACV are not a small detail

Replacement Cost Value (RCV) and Actual Cash Value (ACV) sound technical. They are not. They decide whether the insurer pays for a new equivalent item or pays a reduced amount after depreciation.

Here's the clean comparison:

| Feature | Replacement Cost Value (RCV) | Actual Cash Value (ACV) |

|---|---|---|

| Payout basis | Cost to replace with new item of similar quality | Replacement cost minus depreciation |

| Best use | People who want stronger rebuild or replacement protection | People prioritizing lower premium over payout quality |

| Claim result | Usually leaves a smaller financial gap | Usually leaves a larger financial gap |

| Premium impact | Typically higher | Typically lower |

| Renovation risk | Better fit when material and labor costs are moving up | More likely to leave you short after a major loss |

Now put that into a renovation context. Say a storm damages part of an older roof while your addition is underway, or a covered event destroys flooring you hadn't planned to replace yet. With RCV, you're generally aiming for replacement with new materials of similar quality. With ACV, age and wear reduce the payout. That difference can force you to fund the gap yourself while your project is already over budget.

If your budget only works when the claim pays near full replacement, ACV is the wrong bet.

Underinsurance often creates significant problems. People trim costs by accepting lower limits, more ACV treatment, or both. Then labor and material prices move the wrong way, and the policy no longer reflects reality. You don't notice until there's a claim.

My advice is simple. For any major renovation, review the dwelling limit, ask exactly how losses are settled, and don't assume upgraded finishes are automatically reflected in your policy the moment you pay the contractor deposit.

Plugging the Gaps Common Exclusions and Endorsements

A lot of people think a “good” policy covers basically everything except obvious edge cases. That's wrong. Standard policies are designed with intentional gaps.

Rutgers' analysis describes a protection gap in homeowners insurance because people often assume the policy covers risks like flood when it does not, or they don't understand how policy restrictions reduce what a claim will pay, as explained in Rutgers' review of protection gaps in homeowners insurance.

The exclusions people assume away

The big ones are the ones people mention after a disaster, not before one:

- Flood: Standard homeowners insurance generally doesn't cover flood damage.

- Earthquake: Usually excluded unless you buy separate coverage.

- Sewer or water backup: Often requires an endorsement.

- Slow leaks or maintenance-related damage: Insurers commonly treat wear, neglect, or gradual damage very differently from sudden accidental loss.

- War and nuclear accident: These are classic major exclusions in standard policy forms.

The renovation angle is what makes this more dangerous. A project can expose hidden plumbing issues, drainage problems, and structural vulnerabilities. Then a homeowner learns that the loss wasn't excluded because the insurer is evil. It was excluded because the base policy was never meant to be all-risk in the way people imagine.

Endorsements are how you tailor the policy

Endorsements are the fix. Think of them as targeted upgrades to your policy, not optional fluff.

You might need them for:

- Water backup risk: Especially if the project affects plumbing, drains, or basements.

- High-value items: Jewelry, art, or collectibles can outgrow standard sublimits.

- Higher rebuild expectations: Added value from renovations may require updated limits or inflation-sensitive features.

- Project-specific exposure: Some renovations justify asking whether temporary construction-related coverage is needed.

The mistake isn't failing to buy every add-on. The mistake is assuming the base policy is already all-encompassing. It isn't. It's a starting point.

Insurance and Home Projects Protecting Yourself From Contractor Risk

This is the part people get wrong because they trust the contract more than the insurance. A signed renovation agreement does not magically protect you from the contractor's mistakes, uninsured subs, or disputed responsibility.

Your homeowners insurance coverage protects your property interests. The contractor's insurance protects against liabilities they create. Those are related, but they are not the same thing.

Your policy and the contractor's policy do different jobs

If a contractor causes water damage while relocating a line, their general liability policy may be the first place to look. If a worker gets injured on your property, the contractor's workers' compensation coverage matters because you do not want that claim looking for a home under your own liability situation.

This gets messy fast when the contractor is sloppy about paperwork or uses subcontractors you never vetted. The best time to discover that is before demo, not after a ceiling collapse.

What I recommend is simple and essential: verify the contractor's insurance yourself. Don't accept “we're fully insured” as an answer. That phrase is worth nothing without documents and confirmation.

What to demand before work starts

Ask for these items in writing:

A current Certificate of Insurance

Make sure it shows the business name that matches your contract, not some related entity you've never heard of.Proof of general liability coverage

This is the policy you care about when the contractor damages your property or someone alleges the business caused harm.Proof of workers' compensation coverage

If there are people swinging hammers at your house, this matters.Your project address tied to the job records when appropriate

The cleaner the paper trail, the less room there is for finger-pointing later.Direct verification from the issuing agent or broker

Call the contact listed on the certificate and confirm the policy is active. Certificates can be outdated. They can also be misleading if you never verify them.

Ask one blunt question: “If your crew damages my house or a worker gets hurt here, which policy responds first?”

If the contractor hesitates, gets defensive, or tells you this is “standard stuff you don't need to worry about,” slow the project down.

A few more smart moves:

- Tell your own insurer about the project: Especially if it's structural, involves additions, or significantly changes the home's value.

- Ask whether the renovation triggers any underwriting concerns: Some insurers care about vacancy, roof work, major system changes, or long project timelines.

- Find out whether specialty construction coverage is needed: For larger jobs, builder's risk or similar project-specific coverage may make sense.

If you want a cleaner way to start, using a renovation match through Handvetted helps cut down the screening burden because the professional arrives pre-checked instead of self-described.

Navigating a Claim When Something Goes Wrong

Claims go better when you act fast and stay organized. They go worse when you clean up first, document later, and rely on memory.

If something happens during a renovation, your job is not to become a claims expert overnight. Your job is to create a clean record, prevent additional damage, and avoid saying sloppy things that complicate coverage.

What to do in the first hour

Start here:

- Stop the damage if you safely can: Shut off water, secure openings, and take reasonable steps to prevent further loss.

- Document before cleanup: Take photos and video from wide angles and close range.

- Save damaged materials when practical: Don't throw away the evidence before the adjuster sees it.

- Notify the right parties quickly: Your insurer, the contractor, and if needed the contractor's insurer.

Write down what happened in plain English while it's fresh. Time, location, sequence, who was present, what work was happening. That short note can be more useful than a long emotional explanation three days later.

How to deal with the claim without making it worse

Be factual. Don't guess at cause if you don't know it yet. Don't exaggerate. Don't minimize either.

If the contractor may be responsible, send written notice to the contractor right away and keep everything in email if possible. If emergency drying, board-up, or mitigation work is needed, use a reputable professional and keep every invoice, photo, and communication. If you need help fast, a damage restoration match through Handvetted can shorten the scramble.

The best claim file is boring. Clear photos, dated notes, invoices, names, and no drama.

One judgment call matters. Not every small loss should become a claim. If the damage is modest and comfortably payable out of pocket, think carefully before filing. Insurance is there for meaningful risk transfer, not every nick and dent of a project. But for major losses, don't delay. Late reporting creates problems you do not need.

A Pre-Project Checklist to Manage Coverage and Costs

Home insurance costs have climbed hard. LendingTree reports that rates rose a cumulative 46.8% nationally between 2020 and 2025, with 2025 alone up 6.0% and no state seeing a decline that year. The same analysis puts the average annual U.S. premium at $2,395, with Oklahoma at $5,298, or 121.2% above the national average, and Hawaii at $801, as shown in LendingTree's state-by-state home insurance analysis. That's why managing homeowners insurance coverage before a renovation is not optional.

The answer isn't “buy everything.” The answer is to tighten the policy where it matters and stop paying for coverage you haven't reviewed.

The smartest moves before demo day

Use this checklist before work starts:

- Review the dwelling limit: Make sure it reflects the home you're about to have, not the one you had two years ago.

- Check settlement method: Confirm whether key parts of your policy pay on an RCV or ACV basis.

- Read the exclusions that match your project: Water backup, flood, earthquake, and gradual damage are the usual trouble spots.

- Ask your insurer about the renovation: Tell them the scope, cost, timeline, and whether structural work is involved.

- Verify contractor insurance yourself: Certificate of Insurance, active policies, and direct confirmation.

- Document the pre-project condition of the house: Photos and video make claim disputes easier to resolve.

- Consider a higher deductible only if you can comfortably absorb it: Lower premium is useless if the deductible creates cash stress later.

- Shop intelligently: Compare on coverage quality, exclusions, and claim settlement. Not just price.

If you do those eight things, you'll be ahead of the curve when starting a project. More important, you'll know where the actual risk sits before anyone swings a hammer.

If you want help finding the right pro before a renovation, claim repair, or insurance review, Hand Vetted Co. is a practical place to start. They match you with one licensed, background-checked, highly rated professional instead of blasting your info to a pile of businesses. That makes the first conversation a lot more useful, and a lot less noisy.

Powered by the Outrank app